What Is Etihad Doing?

There was a time when Etihad Airways looked like it belonged in the same sentence as Emirates without any qualification. It had the swagger, the ambition, and, on the Airbus A380, arguably the most ridiculous commercial flying product ever created: The Residence, a three-room suite in the sky that turned the airline into an object of fascination far beyond Abu Dhabi. Even today, Etihad still describes its A380s as the only aircraft with a three-room suite in the sky.

Then came the retrenchment.

Reuters reported in 2020 that Etihad was considering retiring its A380s early, and by 2021 then-CEO Tony Douglas was saying it was “very likely” the aircraft would never fly for Etihad again. That was not just a fleet decision. It felt like the symbolic end of one version of Etihad: the version that wanted to match or even outdo the grandest instincts of the Gulf megacarriers.

But that decision also reflected the airline’s financial reality at the time.

Between 2016 and 2019 Etihad lost billions of dollars as it unwound an aggressive investment strategy in other airlines like Alitalia and Air Berlin. In 2016 alone the airline posted a $1.9 billion loss, followed by another $1.5 billion loss in 2017. Revenue hovered around $6–7 billion annually, but the company was structurally unprofitable.

During those same years its Gulf rivals were operating on an entirely different scale.

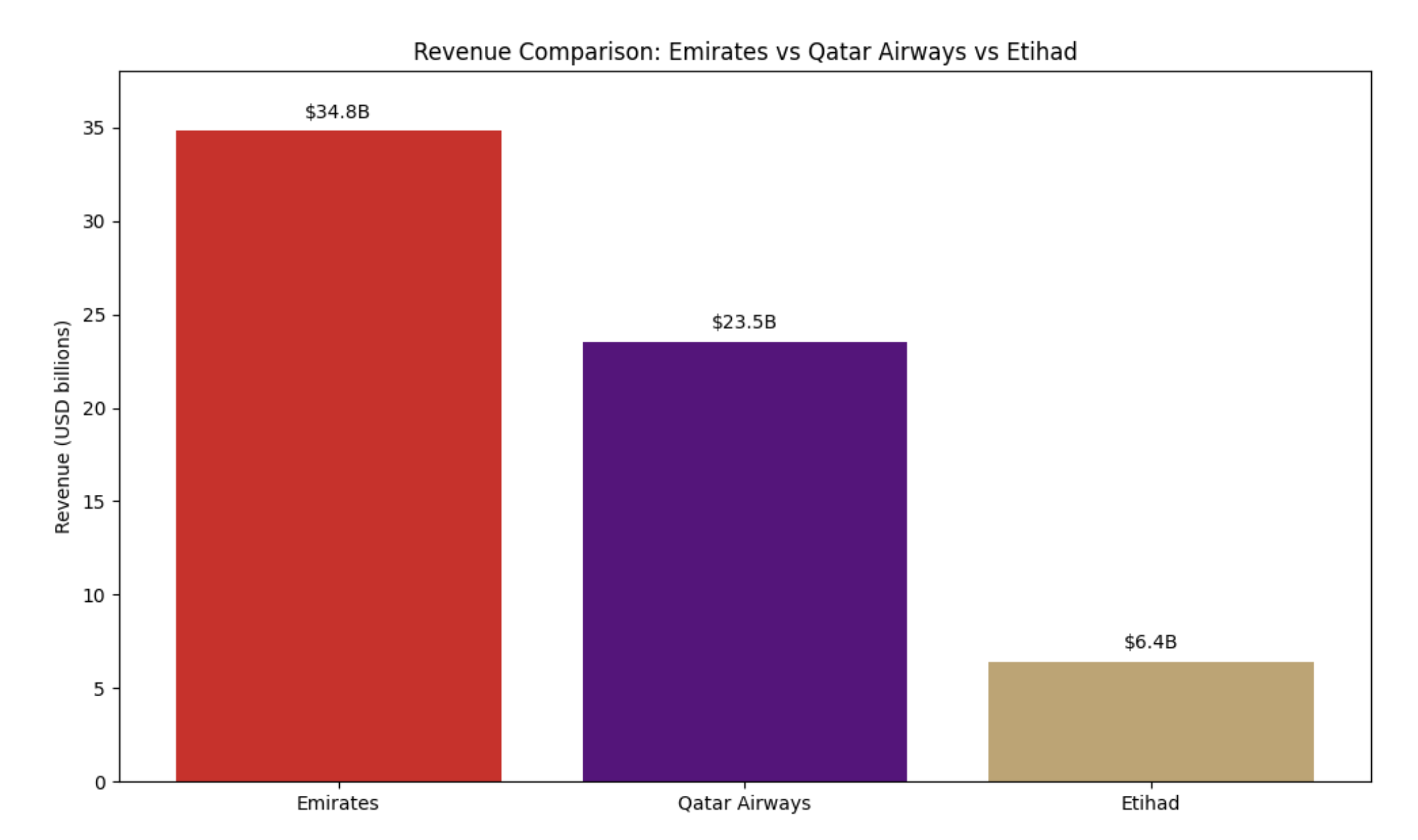

Emirates, the region’s dominant airline, was generating $25–30 billion in annual revenue throughout the late 2010s and remained profitable in most years before the pandemic. Qatar Airways, meanwhile, had built a network nearly as global as Emirates and regularly reported revenues around $13–15 billion, positioning itself firmly between the giant in Dubai and the much smaller Etihad.

In other words, the three airlines that outsiders often grouped together were not actually operating on the same financial level at all.

Emirates was a global aviation giant.

Qatar Airways was a premium-focused challenger.

Etihad was a far smaller airline that had briefly tried to behave like the first two.

Then came COVID, which forced a reset across the entire Gulf aviation sector.

Even Emirates, historically one of the most profitable airlines in the world, posted a staggering $5.5 billion loss in 2020–2021. Qatar Airways reported losses exceeding $4 billion during the same period. Etihad, already in restructuring mode, shrank its network dramatically and accelerated its shift toward a smaller, more disciplined airline.

And yet Etihad never fully committed to becoming something simpler and cleaner either.

In late 2022 it reversed itself and announced the A380 would return. In 2023 the superjumbo came back on London, and in 2024 it expanded to New York. That left Etihad in an odd place: an airline that had publicly declared the economics no longer worked, only to bring back the very aircraft that most powerfully represented its old identity.

The confusion did not stop there.

Etihad’s Boeing 787 fleet has become the backbone of the airline’s long-haul operation, but the carrier presents it primarily as an efficient, business-class-heavy aircraft rather than a true first-class flagship. At the same time, the airline now markets its A321LR as having the world’s only First Suite on a narrowbody aircraft.

So Etihad in 2026 is simultaneously flying:

an ultra-luxury A380 halo product

a large long-haul fleet without a consistent flagship first-class product

a boutique narrowbody first-class cabin that functions mostly as a marketing signal

That mix might sound chaotic, but financially the airline has quietly become far healthier than it was a decade ago.

Under CEO Antonoaldo Neves, who took over in October 2022, Etihad has returned to sustained profitability. The airline reported AED 1.7 billion ($460 million) in profit for 2024 and AED 2.6 billion ($710 million) for 2025, while expanding its fleet to 127 aircraft and carrying 22.4 million passengers.

For context, that still leaves Etihad much smaller than its two Gulf peers.

For context, Etihad remains far smaller than its two Gulf rivals. Emirates generates roughly five times Etihad’s revenue, and Qatar Airways about three times as much. Yet the more interesting development is that Etihad may now be the most structurally disciplined airline of the three. After the failed investment strategy of the 2010s—when it bought stakes in struggling European carriers—the airline pivoted. It abandoned that approach, cut costs, rationalized routes, and refocused on building a sustainable hub airline in Abu Dhabi with a smaller fleet centered on the Boeing 787 and Airbus A350 rather than massive A380 expansion. That shift appears to be working. Reuters has reported that CEO Antonoaldo Neves believes Etihad can now self-fund roughly $20 billion in expansion—something that would have sounded implausible just five years ago.

But stronger finances have not produced a clear identity. Emirates knows exactly what it is: scale, spectacle, consistency, and Dubai. Qatar Airways is equally clear: a relentlessly premium airline centered on Doha with one of the world’s most acclaimed business-class products. Etihad, by contrast, still appears to be experimenting with several identities at once. It wants premium cachet without the cost structure of copying Emirates, efficiency while still investing in symbolic luxury products for branding, and disciplined growth while using Abu Dhabi’s enormous new Terminal A as the base for a much larger airline.

Terminal A may ultimately reshape the equation. The facility can handle roughly 45 million passengers annually—far beyond Etihad’s current traffic—and the airline has described it as the cornerstone of its next growth phase. Expansion has already begun: within a year of the terminal opening, weekly flights increased from 1,336 to 1,732. The infrastructure now exists for Etihad to grow far beyond the boutique-scale carrier it recently resembled.

That creates the central question about the airline’s future. Financially, Etihad now looks like a lean premium carrier—profitable, disciplined, and expanding cautiously. Yet culturally it still gravitates toward the theatrics that defined the Gulf aviation arms race. Reviving The Residence while emphasizing efficient 787 operations and A321LR First Suites sends a mixed signal. The most plausible outcome is that Etihad does not fully return to competing head-to-head with Emirates or Qatar on sheer scale or extravagance. Instead it may evolve into a larger, wealthier, profitable airline that still feels slightly fragmented at the top end: good, sometimes excellent, occasionally fascinating, but not entirely sure which version of itself it wants to be. The recent U.S.–Iran airspace tensions may have exposed short-term fragility in Gulf aviation, but Etihad’s real question predates that crisis: is the airline trying to become great again, or simply trying to remain sustainably profitable?